Copy link

Copy link

The electronic invoice is a document with the same content as a traditional paper invoice, which, however, is presented in digital format and must be signed with a certificate from a recognized certification body.

If we are looking for a specific definition, we can refer to article 1 of Law 56/2007 : "The electronic invoice is an electronic document that complies with the legal and regulatory requirements required for invoices and that also guarantees the authenticity of its origin and the integrity of its content" .

Although there are different mechanisms to guarantee the authenticity of the origin and the integrity of the content from the moment of its issuance until the end of the conservation period, in the case of the electronic invoice the use of the electronic signature is the most widespread.

Likewise, Law 25/2013 on the promotion of electronic invoicing and creation of the accounting register of invoices in the public sector, in article 5. Format of electronic invoices and their electronic signature, indicates that: "...Electronic invoices sent to public administrations must have a structured format and be signed with an advanced electronic signature based on a recognized certificate..."

Electronic invoicing is understood as the process of transmitting invoices between senders and receivers (or similar documents) by electronic means (computer files) and telematics (from one computer to another), digitally signed with recognized certificates and with the same legal validity as invoices issued on paper.

The formats of the electronic invoice can be diverse (xml, edifact, pdf, html, doc, xls, gif, jpeg or txt, among others) as long as the legal content required of any invoice is respected and the requirements for authenticity and integrity are met, for example with the incorporation of a recognized electronic signature.

However, after the publication of Order PRE/2971/2007, which defined the mandatory use of the XML facturae format when the recipient is the General State Administration and its public bodies, this format has also been adopted by other administrations and frequently, among private companies.

It is worth noting that Law 25/2013, in the second additional provision, states: "...electronic invoices sent to public administrations must conform to the structured format of the electronic invoice Facturae, version 3.2" , thus establishing the format of electronic invoices that public administrations must admit in their invoice register.

On the other hand, it is necessary to bear in mind the Resolution of March 21, 2014, of the Undersecretariat, by which the Resolution of March 10, 2014, of the Secretariat of State for Telecommunications and for the Information Society and of the Secretaries of State for Finance and Budget and Expenditure, by which a new version, 3.2.1, of the facturae electronic invoice format is published.

What is NOT an electronic invoice?

It is important to know what an electronic invoice is and what it is not, since the files we store or send may not have legal validity.

Some examples of documents that are not electronic invoices:

• A digital document in electronic format (pdf, xls, doc, etc.) received by email

• A digital document with a scanned signature

• A digital document signed with a digital certificate not recognized by the AEAT . It must be a recognized certification body.

• A digital document signed with a digital certificate expires , as the certificate is not valid for signing.

In summary, for an electronic invoice to have the same legal validity as an invoice issued on paper, the electronic document that represents it must carry an advanced electronic signature based on a recognized certificate and be transmitted by telematic means.

The electronic invoice within the overall accounting process should not be understood as part of an isolated process, but as an integrated element within the overall financial management of an organization. Broadly speaking, the electronic invoicing process consists of two basic and differentiated processes depending on whether the issuer or recipient of the invoice is involved.

Requirements for issuing invoices:

- Generation of the invoice from the issuer's management systems or from a market platform providing electronic invoicing services with the consent of the recipient.

- Transformation of the issuer's original format into the appropriate invoice format.

- Electronic signature of invoices , directly by the issuer or by a third-party platform using a recognized digital certificate.

- Custody of e-signed invoices or their original matrix by the issuer or electronic invoicing service provider.

- Access, consultation, viewing, printing, signature audit and download of signed invoices within the issuer's system (if you decide to keep the signed invoice) or within the third-party platform.

Requirements for receiving invoices:

- Receipt of invoices in digital format .

- Verification of the e-signature of invoices , either from a local application or through a third-party validation platform.

- Repository and custody of signed invoices in a local application or third-party platform.

- Local application or from electronic invoicing service providers for accessing, consulting, viewing, printing, auditing signatures and downloading signed invoices.

In this way, it is no longer required to print the invoice for it to be legally valid and, above all, its processing (issuance, distribution and conservation) can be carried out directly on the electronic file generated by the issuer.

It should also be noted that all the above obligations can be carried out directly by the taxpayer himself or by a third party, acting in the name and on behalf of the former, with whom he must have the corresponding service provision agreement (regulated in article 5.1 of RD 1496/2003 , where the legislator makes it clear that although sub-invoicing to third parties is permitted, it is the taxpayer who is responsible for fulfilling all these obligations).

Content of invoices.

Royal Decree 1619/2012, of November 30, which approves the Regulation regulating invoicing obligations, in its Chapter II, invoice requirements, in article 6 refers to the content of the invoice in the following terms:

"1. Every invoice and its copies must contain the data or requirements specified below, without prejudice to those that may be mandatory for other purposes and the possibility of including any other mentions:

a) Number and, if applicable, series...

b) The date of shipment.

c) Full name, business name or company name, of both the person required to issue the invoice and the recipient of the transactions.

d) Tax identification number...

e) Domicile, both of the person obliged to issue an invoice and of the recipient of the operations.

f) Description of the operations, providing all the data necessary to determine the taxable base of the tax...

g) The tax rate or tax rates, if applicable, applied to the operations .

h) The tax quota that, if applicable, is affected, which must be entered separately.

i) The date on which the operations being documented were carried out or on which, where applicable, the advance payment was received, provided that this is a date different from that of issue of the invoice.

j) In the event that the operation documented in an invoice is exempt from tax, a reference to the corresponding provisions of Directive 2006/112/EC of 28 November on the common system of value added tax, or to the corresponding provisions of the Tax Law or an indication that the operation is exempt..."

Preservation of the electronic invoice.

The recipient of the electronic invoice must keep it as it was transmitted to him , on an electromagnetic or optical medium and must have computer means that allow him to verify its authenticity and integrity.

The electronic invoice format defined by the General State Administration and implemented in the e-FACT service of the AOC Consortium is XML with a specific structure known as factura-e .

Currently, the versions of Facturae accepted by the e-FACT service, in accordance with Law 25/2013, of December 27, on the promotion of electronic invoicing and creation of the accounting register of invoices in the Public Sector , are 3.2, 3.2.1 and 3.2.2.

If invoices are sent in an older format, they will be rejected.

You can obtain more details about the format and versions in the document Formato Facturae on the website http://www.facturae.es .

Yes . The Generalitat de Catalunya has declared the e-FACT service as the General Invoice Entry Point for Catalan public administrations through agreement 151/2014, of 11 November, on the general entry point for electronic invoices in Catalonia, published in DOGC no. 6747, of 13 November 2014.

Documents of interest:

Agreement 151/2014, of November 11, on the general entry point for electronic invoices in Catalonia

- Yes , the e-FACT complies with the requirements of Order HAP/1074/2014, of June 24 , which regulates the technical and functional conditions that the general point of entry for electronic invoices must meet. In this regard:

- The protocol used by the AOC Consortium (FTP / SFTP) for the automatic sending of electronic invoices from the supplier's invoice management systems, perfectly complies with the definition of international organizations (W3C) on web services interfaces. Web services are a set of protocols and standards that aim to exchange data between applications, although among the main ones is SOAP, many others are recognized.

- In relation to the requirement of Order HAP/1074/2014 that communications between the provider's system and the service be signed by a certificate owned by the provider or owned by a third party other than the provider with whom the electronic invoicing service is contracted, the e-FACT service allows the use of the SFTP protocol which incorporates the use of cryptography, with a public key system to provide security and confidentiality to transfers.

- The technical conditions of "the resolution of October 10, 2014, of the Secretariat of State for Public Administrations" only apply to the general point of entry of electronic invoices of the General State Administration, as stated in point 1) of the resolution and, therefore, do not affect the e-FACT.

Objective

Incorporate the necessary adaptations to the General Invoice Entry Point (PGE, hereinafter) of the e-FACT service to comply with the requirements imposed on the PGE as established in Order HAP/1650/2015, of July 31, which modifies Order HAP/492/2014, of March 27, which regulates the functional and technical requirements of the accounting register of invoices of entities within the scope of Law 25/2013, of December 27, on the promotion of electronic invoices and the creation of the accounting register of invoices in the public sector, and Order HAP/1074/2014, of June 24, which regulates the technical and functional conditions that the general point of entry of electronic invoices must meet : https://www.boe.es/diario_boe/txt.php?id=BOE-A-2015-8844

Description of validation rules

In the document you will find information about who is responsible for carrying out the validations (e-FACT as PGE or the invoice accounting records (RCF) of the entity receiving the invoice).

Recommendations regarding the order in which to apply validations

- It is recommended to follow the sequence

- It is recommended to perform all validations to return all detected errors to the supplier, except for the following:

- If validation 6a relating to the number of decimals is not passed, validation 6a relating to the calculation of the total cost and gross amount is not continued.

- If validation 6b regarding the number of decimal places is not passed, validation is not continued.

E-invoice format recommendations 3.2.1 for the application of these validations

Given that the accounting validations in section 6 of the order involve calculations of amounts, we recommend sending invoices in format 3.2.1 for greater precision in the case of amounts with fractions and thus avoid rejections due to incorrect rounding required by the e-invoice format 3.2.

How are RCF rejects returned to the PGE?

When an invoice is rejected for not complying with the validation rules, all these errors have been grouped in the code =HF09 and the description includes the specific error code and its description. All errors detected are returned in the following format:

- "Error code: Description | error code: Description"

For example, in an invoice with validation errors detected RCF05002 and RCF05004, the following would be returned as a rejection comment:

- RCF05002: Issuer: The NIF does not comply with the rules and criteria for its formation. Rule number 5b of Annex II of Order HAP / 1650/2015 is not complied with | RCF05004: Issuer: The name and first surname are mandatory. Rule number 5d of Annex II of Order HAP / 1650/2015 is not complied with |

It should be noted that the size of this field is 500 characters and if the sum of the errors exceeds this threshold, the error message will be truncated when character 500 is reached.

Description of validation errors

| Code | Error description | Implementation date in the PGE |

| RCF03001 | The invoice number is mandatory. Rule 3a of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF04001 | Rectifying invoice with rectification criteria other than 01,02,03,04. Rule 4a of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF04002 | For rectification invoices with rectification criterion 01 or 02, the invoice number of the issuing issuer is mandatory. Rule 4b of Annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05001 | Issuer: The code of type of person, physical \"F\" or legal entity \"J\" is mandatory. Rule 5a of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05002 | Issuer: The NIF does not conform to the rules and criteria of its formation. Rule 5b of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05003 | Issuer: The country code (two first characters of the NIF when they are letters) when it exists, will be adjusted to what is established in the Invoice scheme itself. Rule 5c of Annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05004 | Issuer: Number and first name are mandatory. Rule 5d of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05005 | Issuer: The company name is mandatory. Rule 5e of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05006 | Assignee: The code of type of person, physical \"F\" or legal entity \"J\" is mandatory. Rule 5a of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05007 | Assignee: The NIF does not conform to the rules and criteria of its formation. Rule 5b of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05008 | Assignee: The country code (two first characters of the NIF when they are letters) when it exists, will be adjusted to what is established in the Invoice scheme itself. Rule 5c of Annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05009 | Transferee: The number and first name are mandatory. Rule 5d of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF05010 | Assignee: The company name is mandatory. Rule 5e of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF06001 | In the invoices issued in euros, some of the line amounts have more than two decimal places or are not numeric. Rule 6a of Annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF06002 | In invoices issued in euros, the total cost of each line must be equal to the product of the number of units by the unit price rounded with the common method of rounding to two decimal places. Rule 6a of Annex II of Order HAP/1650/2015 is not complied with | From 03/05/2017 |

| RCF06003 | In invoices issued in euros, the gross amount of each line must be the sum of the total cost plus the sum of surcharges minus the sum of discounts. Rule 6a of Annex II of Order HAP/1650/2015 is not complied with | From 03/05/2017 |

| RCF06004 | In the invoices issued in euros, some of the amounts at the invoice level, except the tax rates or the percentages to be applied, have more than two decimal places or are not numerical. Rule 6b of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF06005 | In invoices issued in euros, the total gross amount of the invoice must be the sum of the gross amounts of the lines. Rule 6b of annex II of Order HAP/1650/2015 is not complied with | From 03/05/2017 |

| RCF06006 | The currency code is not valid. The rule is broken. Rule 6c of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF07002 | The date of issue of the invoice is mandatory and must be a valid date. Rule 7a of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF09002 | There are invoice lines without content in the description. Rule 9b of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF01001 | The invoice does not comply with the "Facturae" XSD schema of the corresponding version (3.2 or 3.2.1). Rule 1 of annex II of Order HAP/1650/2015 has been breached | 03/15/2017 |

| RCF02001 | Invalid signature: Certificate currently expired in a non-long-lived signature. Rule 2 of annex II of Order HAP/1650/2015 is breached | 03/15/2017 |

| RCF02002 | Invalid signature: Certificate currently revoked in a non-long-lived signature. Rule 2 of annex II of Order HAP/1650/2015 is breached | 03/15/2017 |

| RCF02003 | Invalid signature: Invalid certificate. Rule 2 of annex II of Order HAP/1650/2015 is breached | 03/15/2017 |

| RCF02004 | Invalid signature: Untrusted certificate. Rule 2 of annex II of Order HAP/1650/2015 is breached | 03/15/2017 |

| RCF02005 | Invalid signature: Integrity error. Rule 2 of annex II of Order HAP/1650/2015 is breached | 03/15/2017 |

| RCF02006 | Invalid signature: Invalid signature format. Rule 2 of annex II of Order HAP/1650/2015 is breached | 03/15/2017 |

| RCF02010 | The invoice does not contain signatures: Rule 2 of Annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF09001 | The registration number assigned at the general entry point for electronic invoices is mandatory. Rule 9a of Annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

| RCF07001 | The date of entry in the administrative register is mandatory, it must be valid, prior to or equal to the current date and greater than or equal to the date of issue of the invoice. Rule 7a of annex II of Order HAP/1650/2015 is not complied with | 03/15/2017 |

The administration that wishes to use the e-FACT service must carry out the following actions:

- Accept the receipt of invoices in electronic format through the e-FACT service for any supplier company by accepting the terms of service .

- Fill out the corresponding service registration form , where the access methods and selected functionalities will be specified.

- Publish a link to your electronic headquarters of the e-FACT service invoice delivery mailbox , or provide an equivalent mechanism that guarantees that any supplier company can send invoices in electronic format to the receiving body at no cost.

- Comply with the following legal obligation :

- Electronic invoice entry registration

- Report on the processing status of invoice management and entry registration data through the status information system.

1.Registration

The receiving body entrusts the AOC Consortium with the automatic registration of invoices in the entity's own registry, which has been duly integrated into the unified registry service (MUX) of the AOC Consortium, or in the auxiliary electronic registry of the receiving body enabled in EACAT by default.

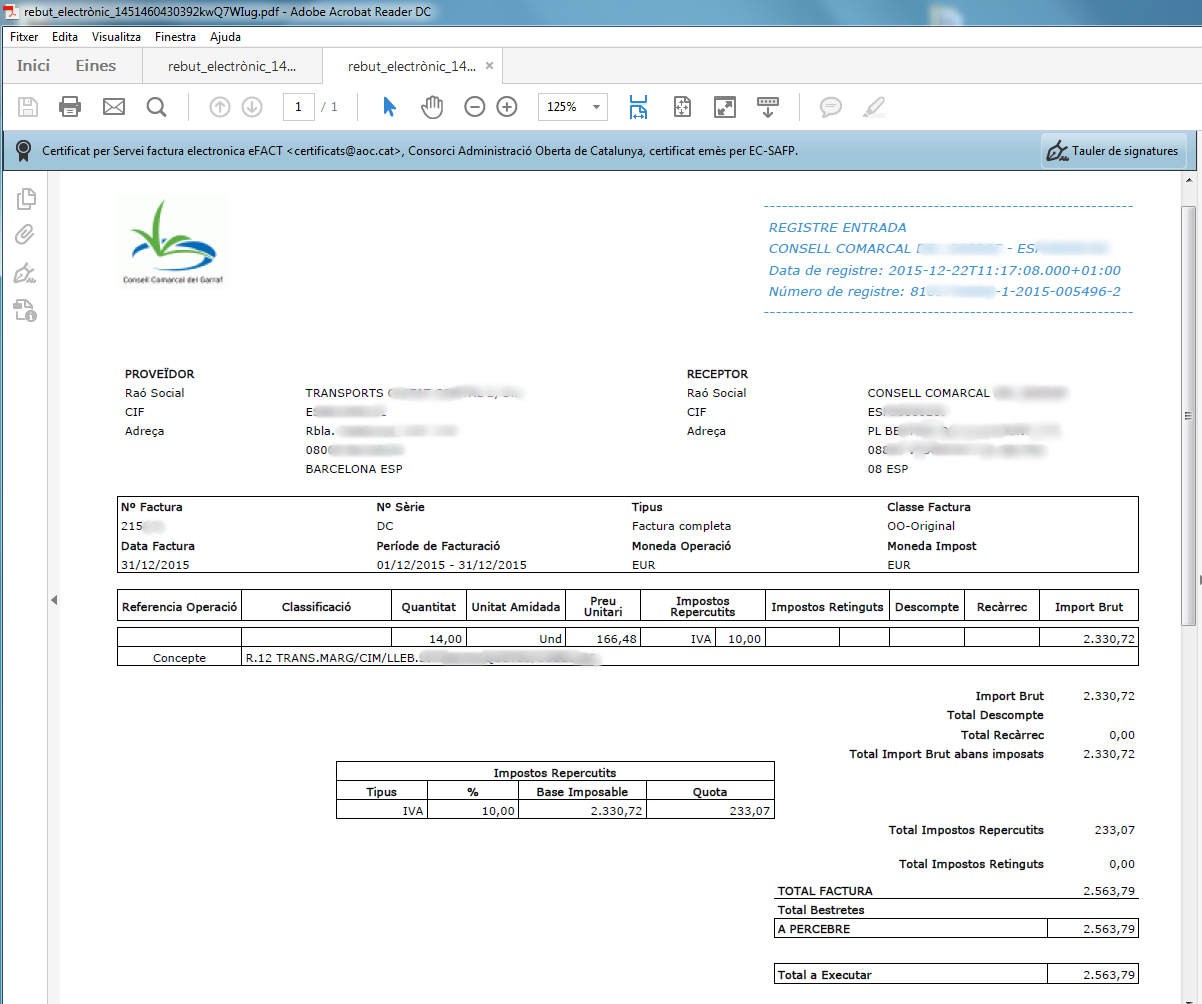

It should be noted that as a result of registration, the e-FACT service generates an electronic receipt . The receipt, which consists of a copy of the invoice in pdf format signed electronically, will be delivered to both administrations and companies, in this case being the guarantee of presentation of the invoice to the recipient.

Below is an example of an electronic receipt issued by the e-FACT service, viewed using Adobe Reader.

Updated information about electronic invoices can be found at: www.facturae.es

This portal dedicated to electronic invoicing contains a specific section of legislative information.

Below we highlight the most relevant legal documents and identify the key aspects that directly affect the electronic invoice:

- The Council of Ministers, at the proposal of the Ministries of Economy and Finance and Industry, Commerce and Tourism, will adopt the necessary measures to facilitate the issuance of electronic invoices for individuals and entities that contract with the state public sector.

- The free support services established for companies must be guaranteed in an Order issued by the Ministry of Economy and Finance.

Royal Decree 1619/2012, of November 30, approving the Regulation regulating invoicing obligations

- Same treatment for paper and electronic invoicing . This equality expands the possibilities for the taxable person to issue invoices electronically without the need for the same to be subject to a specific technology.

- However, to guarantee the legal security of taxable persons who were already using data interchange (EDI) and advanced electronic signature, the Regulation expressly recognizes that said technologies, which are no longer mandatory, guarantee the authenticity of the origin and the integrity of the content of the electronic invoice. Likewise, taxable persons may continue to communicate to the State Tax Administration Agency, prior to their use, the means that they consider to guarantee the aforementioned conditions so that they can be validated by it, if applicable.

- Possibility of electronic submission of invoices or substitute documents and copies thereof with an electronic signature recognized by means of a digital certificate

- Possibility of using electronic invoicing systems based on electronic data interchange (EDI) agreements

- Possibility of receiving electronic invoices from third countries with equal conditions to those required in Spanish territory

- Authorization of electronic invoicing systems at the taxpayer's request

- The use of electronic means for the transmission of electronic invoices to the AAPPs is subject to the express consent of the latter. The consent is general and will extend to all cases in which the recipient of invoices is the recipient.

- Remittance of electronic invoices intended for, or presented to, the AGE or its linked or dependent public bodies, including both in the field of administrative contracting and those issued between individuals, and in the course of any administrative procedure

- Electronic invoices issued by AAPPs will meet the same conditions as those intended for them.

- Standard electronic invoice format (XAdES)

- Boosting the bill in the public and private sector

- More protection for suppliers in their commercial relationships with public administrations, since invoices are presented in an accounting register

- Single point of entry for invoices for each administration (State, Autonomous Communities and Local Entities) in which all invoices from entities, bodies and organizations linked or dependent on that administration will be received.

- Invoices will have a structured format to be specified in a Ministerial Order and signed electronically with a signature based on a recognized digital certificate.

- Mandatory submission of electronic invoices to all taxpayers subject to electronic taxation in accordance with tax regulations from January 15, 2015. However, the administrations may, by regulation, exclude invoices with an amount less than five thousand euros from this obligation.

- All public administrations will be required to have an accounting register of invoices managed by the body responsible for accounting management.

Order HAP/1650/2015, of July 31, which modifies Order HAP/492/2014 , of March 27, which regulates the functional and technical requirements of the accounting register of invoices of entities within the scope of Law 25/2013, of December 27, on the promotion of electronic invoices and the creation of the accounting register of invoices in the public sector, and Order HAP/1074/2014 , of June 24, which regulates the technical and functional conditions that the general point of entry for electronic invoices must meet.

- Obligation to present invoices in an administrative register and identification of bodies

At the Catalan level, the regulations listed below are available.

Law 29/2010, of August 3, on the use of electronic media in the public sector of Catalonia , establishes in its sixth final provision the use of electronic invoices in the following terms:

- The Administration of the Generalitat must promote the use of electronic invoices among economic actors in Catalonia

- The Generalitat must collaborate with the General State Administration in promoting the use of electronic invoices

- The entities that make up the public sector of Catalonia must guarantee the acceptance of electronic invoices within six months of the entry into force of this law and must promote its extension among their suppliers.

Law 10/2011, of December 29, on simplification and improvement of regulatory regulation , defines in the Fourth Additional Provision on the promotion of electronic invoicing:

- With the aim of making the determinations of Law 29/2010, of August 3, on the use of electronic means in the public sector of Catalonia fully effective, public sector entities in Catalonia must promote the use of electronic invoicing as a condition for the execution of public sector contracts.

- Establishes that the e-FACT service of the Open Administration Consortium of Catalonia is the general entry point for electronic invoices of the Autonomous Community of Catalonia, in accordance with article 6.1 of Law 25/2013, of December 27, on the promotion of electronic invoices and creation of the accounting register of invoices.

Source: Electronic invoice guide , Generalitat de Catalunya and General Council of Chambers of Catalonia

- Collection of state regulations: http://www.facturae.gob.es/factura-electronica/Paginas/repertorio-legislativo.aspx

- Collection of regional regulations: http://dogc.gencat.cat/ca/pdogc_canals_interns/pdogc_resultats_fitxa/?documentId=674751&action=fitxa

- Collection of state, regional and European regulations: http://bit.ly/guiaefactura (ANNEX. Legal framework for electronic invoices)